Why You're Getting Flooded With Junk Mail After Your Home Loan Closes (And How to Stop It)

Why Your Mailbox Exploded After Closing Day

You signed the final papers. The keys are in your hand. Your mortgage, home equity loan, or HELOC is officially closed. So why does your mailbox suddenly look like it's been targeted by every financial services company in North America?

The answer is less dramatic than it sounds, but equally frustrating: when you close a major loan, your information travels.

Here's what happens behind the scenes. Credit bureaus flag recently-closed mortgages or other home loans as significant financial events, which signals to lenders and marketers that you're a "hot prospect" for refinancing, more home equity products, or related services.

Think of it this way: you just demonstrated you can qualify for a large loan. To the financial industry, that makes you incredibly valuable. So they buy the right to contact you.

The bottom line? Your mailbox explosion isn't a mistake; it's the predictable result of how the unfortunate side of how the lending industry operates. But not all that mail is created equal, and some of it is genuinely dangerous.

Red Flags: Spotting Predatory Junk Mail and Scams

Not every piece of unsolicited mail is harmless. Some are specifically designed to trick you into paying for services you don't need, giving up personal information, or worse, signing documents that could damage your finances. Here's what to watch for.

Fake Loan Payoff Offers

These arrive with official-looking letterhead claiming they've reviewed your loan and found a way to pay it off early or refinance at a lower rate. The catch? They're trying to get you to apply for a new loan (often with worse terms) or to pay an upfront "processing fee" that never results in anything.

Red flag language: "We've reviewed your account and found exclusive savings," "Act now before this offer expires," or "limited-time opportunity based on your credit profile."

Legitimate lenders don't "review" your account unsolicited and then contact you about mysterious savings. They market openly, without pressure tactics.

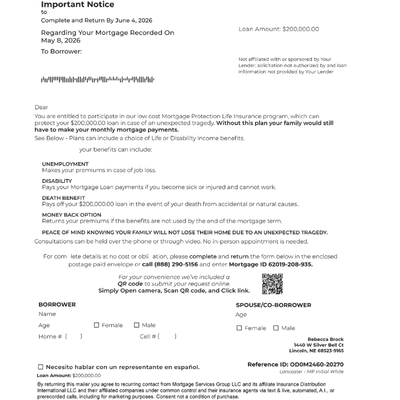

Mortgage Protection and Payment Protection Plans

These scams promise to make your loan payments if you lose your job, become disabled, or face other hardships. The problem? They're expensive, often overlap with insurance you already have, and sometimes have so many exclusions they're nearly worthless when you actually need them.

Scammers use fear to exploit homeowners with urgency just after closing on a large loan. They make it sound essential. It usually isn't.

Red flag language: "Protect your family and your home," "Peace of mind," "What if you lost your job tomorrow?" These emotional appeals (rather than straightforward benefit explanations) are classic scam tactics.

Title Insurance Upsells

For mortgages You already paid for title insurance at closing. That's mandatory. So when you get mail offering "additional title protection" or "title insurance updates," it's junk. Your title insurance doesn't expire, and you don't need a second policy from a random company.

Red flag: If you don't recognize the sender and they're selling title-related products, delete it, throw it in the fire pit or the shredder, or shred it at a free shred day.

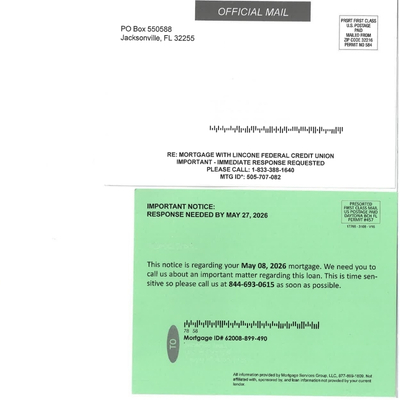

Refinancing Schemes and Rate Lock Offers

Some mailers claim they can lock in your current rate before rates rise, or guarantee approval for a refinance. Real refinancing takes actual application and underwriting, not a mail-in card and a fee.

Occasionally, these mailers are from legitimate lenders, but the language is deliberately designed to create urgency and confusion. Many homeowners respond thinking they're locking something in, when they're just authorizing a credit pull and a sales call.

The Generic Address and Sender Red Flags

Scam mail often comes from PO boxes, generic addresses, or company names that sound official but aren't actually established institutions. Look for:

- PO box addresses instead of street addresses

- Phone numbers that route to call centers (not local numbers)

- Generic sender names like "Mortgage Services" or "Home Equity Solutions"

- No clear company registration or website information

- Misspellings or unusual formatting (scammers sometimes rush)

Examples of Actual Junk Mail

Legitimate Mail From Your Credit Union: What Actually Matters

Not all the mail landing in your inbox is junk. Some of it is genuinely important and comes directly from your credit union or the institution that serviced your loan. Here's what legitimate correspondence looks like.

Loan Closing Documents and Final Statements

Immediately after closing, expect official documentation from your credit union confirming the loan is closed. This includes the final statement showing your payoff amount, the date the loan was satisfied, and details about any remaining credits or fees. These documents are important for your records, keep them.

What to expect: Official letterhead from your credit union, your loan number prominently displayed, clear itemization of final amounts, and a definitive statement that the loan is "closed" or "satisfied."

Tax Documents (Form 1098)

If you made mortgage interest payments in 2025 and closed the loan in 2026, you'll receive a Form 1098 (Mortgage Interest Statement) from your lender by January 31st of the following year. This is required for your taxes if you itemize deductions.

What it looks like: Official IRS form with your credit union's name and EIN (Employer Identification Number), your loan number, and the total interest paid during that tax year. The form will clearly state it's for tax purposes.

Account Statements and Balance Confirmations

If you have other accounts with your credit union (checking, savings, or a home equity line of credit you kept open), you'll continue receiving statements. These are standard and legitimate.

Legitimate Refinancing or Product Offers From Your Credit Union

Your actual credit union may reach out about refinancing options or other financial products they offer. The key difference between this and scam mail?

- It comes directly from your credit union's official address

- It addresses you by name and references your specific account relationship

- It offers clear terms and rates without high-pressure language

- You can easily verify it by calling your credit union's main line (not a number on the mailer)

If your credit union sends a refinancing offer, you can call their main number, ours is 402.441.3555, to confirm it's legitimate before responding.

Important Notices About Policy Changes or Account Updates

Your credit union may send notices about changes to their policies, privacy practices, or account features. These are genuine and sometimes require your attention (especially if they ask you to opt out of something).

How to verify: Check your credit union's website or call them directly. Legitimate notices will match what you see on their official channels.

How to Tell the Difference: A Side-by-Side Comparison

Here's a practical way to evaluate any piece of mail that arrives after your mortgage closes:

| Characteristic | Scam/Junk Mail | Legitimate Credit Union Mail |

|---|---|---|

| Sender Address | PO box, generic address, or difficult to verify | Street address matching your credit union's headquarters or branches |

| Company Name | Generic ("Mortgage Solutions," "Home Services"), similar to but not exactly your lender's name | Your credit union's official, recognizable name |

| Personalization | "Dear Homeowner" or vague references; no specific account details | Addressed to you by name; includes your loan or account number |

| Urgency Tactics | "Limited time," "Act now," "Offer expires," "Must respond by [date]" | No artificial urgency; clear information about actual deadlines (if any) |

| What They're Asking | Upfront fees, personal information, authorization to pull credit, signed documents | Information you already provided; confirmation of details; action only for specific, documented reasons |

| Professional Quality | Misspellings, unusual fonts, cheap paper, inconsistent formatting | Professional letterhead, consistent branding, official form |

| Verifiability | Hard to verify; phone numbers are often call centers; no website or vague web presence | Easy to verify by calling your credit union's main number or checking their website |

Your gut check: If something feels off, it probably is. And if you're unsure, call your credit union directly using the number on your statements or their website, not the number on the mailer.

Take Action: Stop the Junk Mail Now

You don't have to tolerate a mailbox overflowing with junk. Here's exactly how to reduce the volume, step by step.

Step 1: Opt Out of Credit Bureau Marketing Lists (The Most Effective Solution)

Credit bureaus sell access to your information to marketers. Opting out stops a huge portion of junk mail at the source.

What to do:

- Visit OptOutPrescreen.com (the official credit bureau opt-out portal). This website is run by Equifax, Experian, and TransUnion.

- You can opt out online (temporary, 5-year opt-out) or by mail (permanent opt-out).

- For the most effective results, choose the permanent opt-out by mail. Print the form, sign it, and mail it to the address provided.

- Keep a copy for your records.

This single step will eliminate a significant portion of financial services junk mail within 30–60 days.

Step 2: Contact Your Credit Union Directly

Call your credit union and ask them to:

- Remove you from affiliate marketing lists

- Do not sell or share your information with third parties (if you have that option)

- Flag your account to minimize marketing mail

Tip: Ask to speak with customer service, not sales. Explain that you've recently closed a loan and are receiving excessive marketing mail.

Step 3: Unsubscribe From Individual Mailers (When Safe)

Some legitimate companies include unsubscribe information on their mailers. If you recognize the sender and trust it's legitimate, you can follow those instructions.

Warning: Do not unsubscribe from obvious scam mail. This confirms your address is active and monitored, making you a repeat target.

Step 4: Use USPS Informed Delivery (Optional but Helpful)

The USPS Informed Delivery service lets you preview mail before it arrives. While this doesn't stop junk mail, it helps you identify and discard obvious scams immediately upon arrival.

What to do:

- Sign up for free at InformedDelivery.USPS.com.

- You'll receive daily email previews of incoming mail.

- You can delete previews of known junk right away.

What If You've Already Responded to a Scam?

If you've already opened a suspicious mailer and engaged with it, or worse, provided information or money, don't panic. Here's what to do immediately.

If You Provided Personal Information (SSN, Account Numbers, etc.)

Immediate steps:

- Contact the Federal Trade Commission (FTC). Report the scam at ReportFraud.ftc.gov. This creates an official record and helps law enforcement track patterns.

- Place a fraud alert on your credit file. Call one of the three credit bureaus (Equifax, Experian, or TransUnion) and request a fraud alert. You only need to contact one; they'll notify the others. A fraud alert requires creditors to verify your identity before opening new accounts, which slows down identity theft.

- Monitor your credit reports. Visit AnnualCreditReport.com (the official site for free credit reports) and check for unauthorized accounts or inquiries. Do this immediately and again in 30 days.

- Freeze your credit if necessary. If you suspect serious identity theft (not just a scam inquiry), you can place a credit freeze with all three bureaus. This prevents anyone from opening new accounts in your name without unfreezing your credit first.

If You Paid Money to the Scammer

Take these steps:

- Stop payment immediately if you used a credit card or a credit union account. Contact your bank and credit card company within 24 hours. Request that they reverse the transaction and flag it as fraudulent. Many banks will refund scam charges.

- If you sent a check or money order, call your credit union immediately to place a stop payment (there may be a small fee).

- File a police report. Contact your local police department's non-emergency line and file a fraud report. Get a copy of the report number. This helps with any insurance claims or credit freezes you might need later.

- Document everything. Keep copies of the original mailer, any correspondence, payment confirmations, emails, phone calls, and your police/FTC reports. You'll need this if disputes arise.

- Report to the FTC (as mentioned above). They track scam patterns and can take action against repeat offenders.

If You Authorized a Credit Pull or Started an Application

If you signed an authorization allowing the company to pull your credit, here's what to do:

- Contact the company immediately and request to withdraw your application. Do this in writing (email or certified mail) to have proof of your request.

- Place a fraud alert with the credit bureaus (see above). This alerts creditors that there may be fraudulent activity and forces them to verify identity before approving new accounts.

- Monitor your credit. Watch for unauthorized accounts or inquiries. The credit bureaus will notify you of new inquiries, and you can dispute fraudulent ones.

- Don't engage further. If they call, don't discuss anything. Simply say you've withdrawn your application and don't provide any additional information.

The Important Mindset Shift

If you fell for a scam, you're not alone, and you're not foolish. Scammers spend enormous resources perfecting their tactics to exploit emotion and urgency. The fact that you're taking action now is what matters.

The sooner you report it and secure your credit, the better protected you'll be. Most people who act quickly suffer minimal lasting damage.

Moving Forward: Peace of Mind After Closing

Closing on a home loan is genuinely worth celebrating. You own your home (or are well on your way). That mailbox overflow is just the price of that achievement in today's world, but it's a price you can manage.

The key is being selective. Legitimate mail from your credit union matters. Everything else? Take a quick look, spot the red flags, and toss it.

Start today: Visit OptOutPrescreen.com and opt out of credit bureau marketing lists. That single action will reduce junk mail by 60–70% within two months. Then take five minutes to contact your credit union and ask them to flag your account. Those two steps alone will transform your mailbox from chaos to control.

Your home is yours to enjoy. Your mailbox should be, too. If you receive a mailer, email, or other method of communication that makes you feel unsure, contact your local credit union experts, and we will be happy to help keep you and yours safe!

« Return to "Fraud Prevention Resources"

- Share on Facebook: Why You're Getting Flooded With Junk Mail After Your Home Loan Closes (And How to Stop It)

- Share on Twitter: Why You're Getting Flooded With Junk Mail After Your Home Loan Closes (And How to Stop It)

- Share on LinkedIn: Why You're Getting Flooded With Junk Mail After Your Home Loan Closes (And How to Stop It)